Advanced acquiring

1. Introduction

What happens when your customer pushes the pay button? In this video, watch Stella as she explains how you can leverage your authorisation data to optimise your payment process.

This guide will also explain in further details the different stakeholders involved, the role of the acquirer and how the authorisation ecosystem works.

2. What is an authorisation?

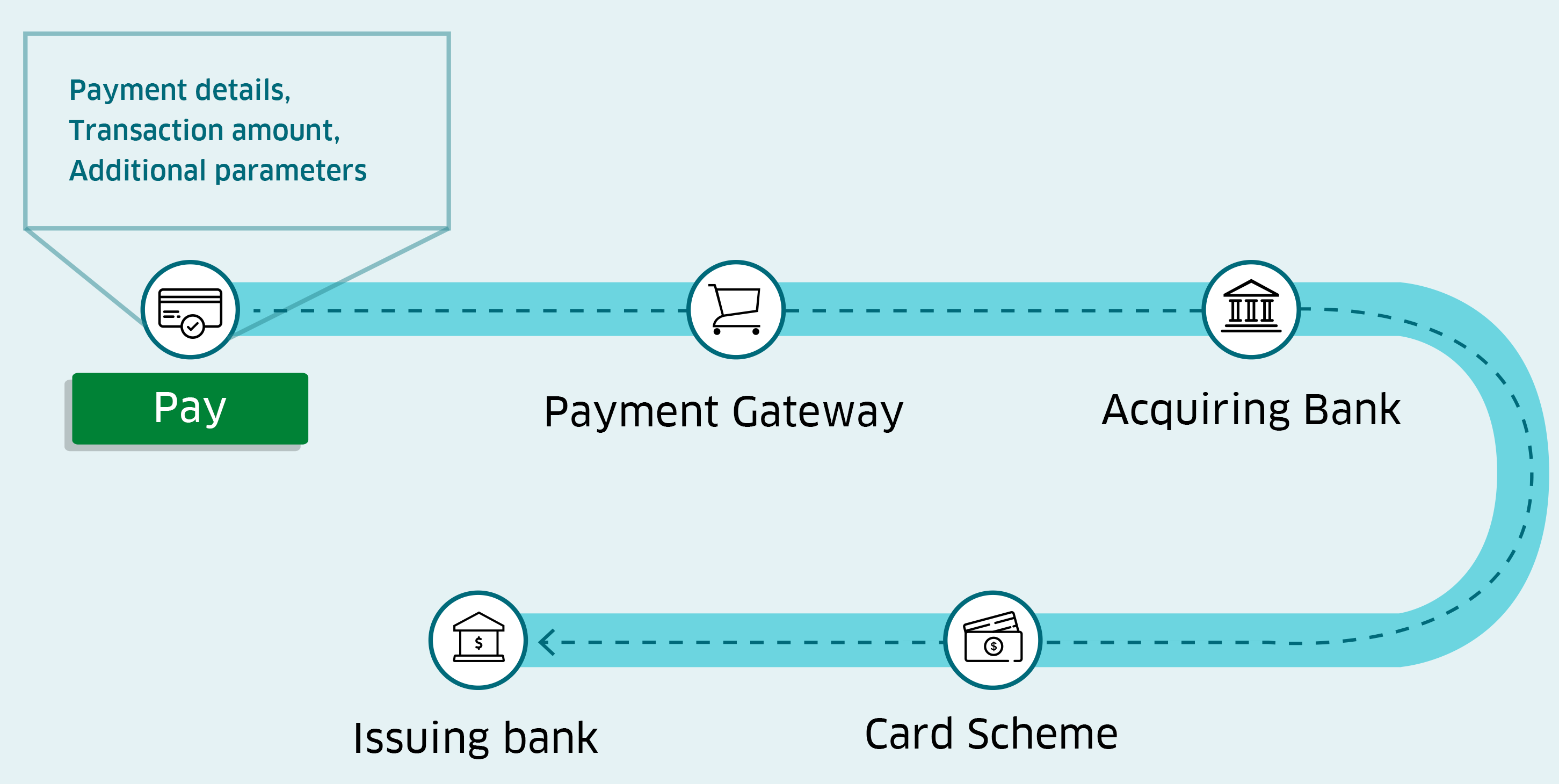

The moment your customer pushes the Pay button, a request to authorise their transaction happens from the payment gateway to the customer's issuing bank (the issuer) via your acquiring bank (the acquirer) and the payment schemes. The authorisation request contains information such as the payment details, transaction amount and additional parameters. The issuer uses it to verify the transaction. These steps happen behind the scenes for your customer.

In most cases, it is the issuer who will accept or decline a transaction based on hundreds of variables. These variables could be transaction data, card information or merchant data.

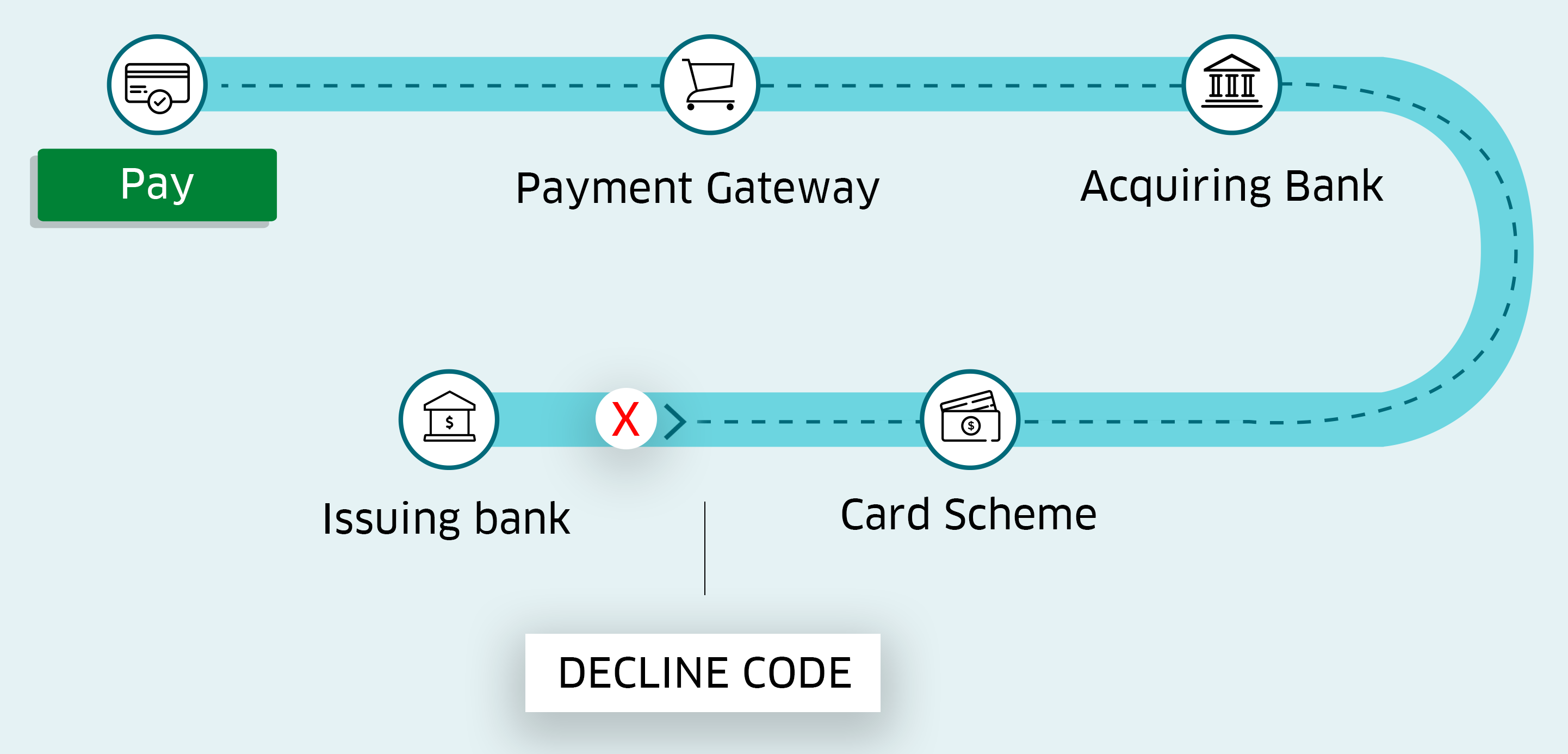

If the transaction is rejected, the issuer will respond with a decline error code in the Back Office. This code describes the reason for rejection such as insufficient funds on the account, blocked card and so on. If you want to understand your acceptance rates, it is important to look at your decline code distribution. To find out more about rejection reasons and what they mean, please read our guide.

3. Full Service offering

All businesses need an acquirer to be able to process card payments. For instance, if you are using a gateway model with us, you would have signed an agreement with an acquirer to be able to accept payments on your webshop.

At Worldline, we also offer the Full Service model. This means that you will only need to sign one contract with us for all your payment needs and we take care of the acquirer agreement on your behalf. This simplifies the setup of your business and makes your daily operations easier.

We also go a step further in the value chain by leveraging the power of our in-house acquirer, Bambora, to continuously improve the transaction flow and offer you the best level of service. Having an in-house acquirer allows us to have more control over the end-to-end customer experience. Thanks to this tight collaboration, we can better support you in optimising your setup, give you access to qualitative and actionable insights as well as to simplify your day to day business.

4. Manage your performance proactively

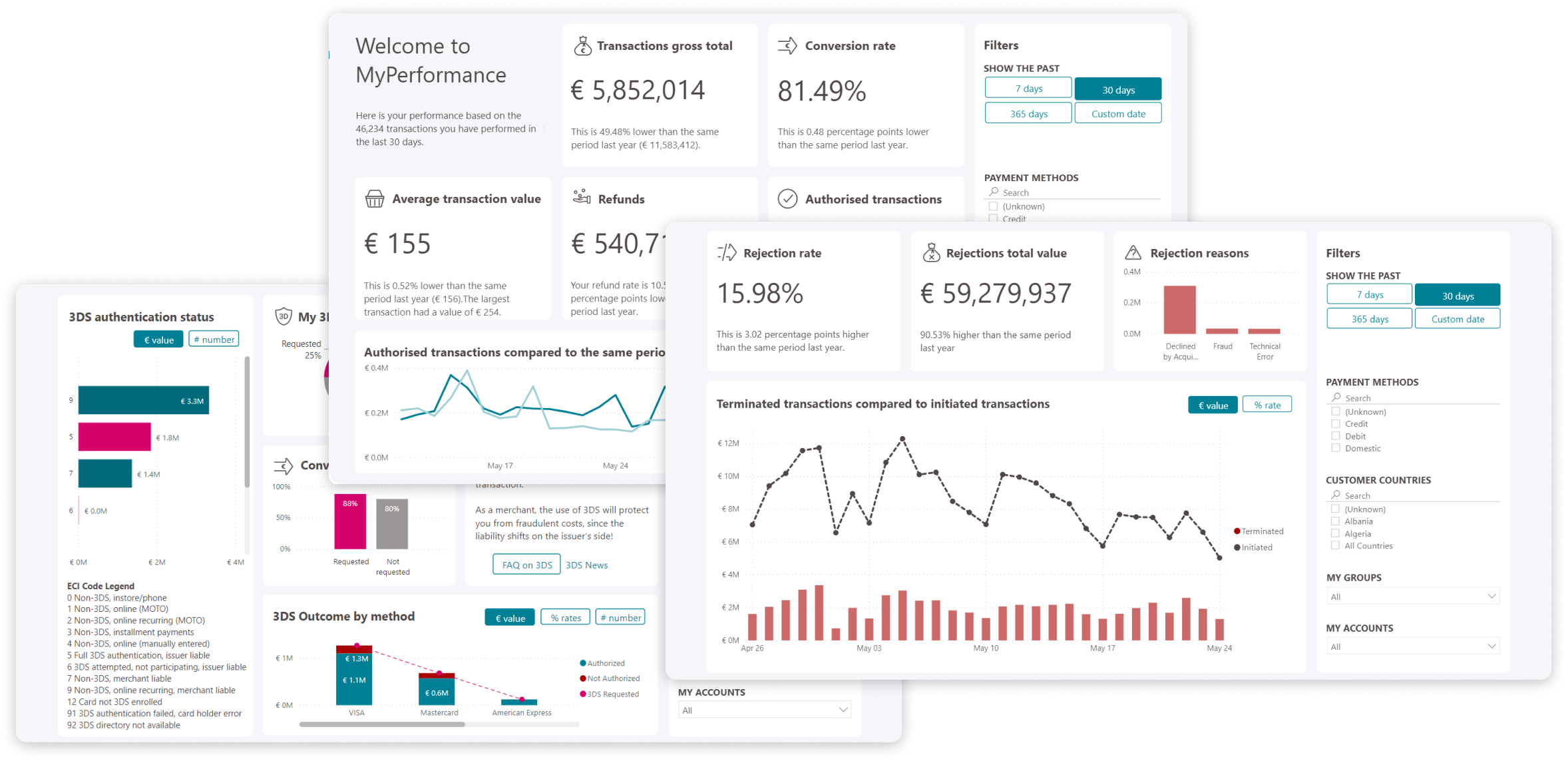

Effective management of performance is essential to any business. However, this can sometimes be difficult to get right. At Worldline, we provide you a suite of tools that will help you keep one step ahead of your business. For example, you can do so by learning about your authorisation acceptance rates and rejection reasons that we make accessible to you. We also give you more details about the way to interpret this information and which actionable insights to implement. It could be simple things like identifying that you have low conversion on foreign cards. You could then remind foreign buyers to allow their settings to support cross-border purchases.

Our Business Intelligence tool, MyPerformance brings together your payment performance insights on one intuitive platform, making it easier for you to stay on top of your business. Get instant access to key metrics like your customer's average transaction value, 3-D Secure requests, refunds and conversion rates over multiple timelines. Read our guide to find out more about MyPerformance and its features.

Upon request, our Payment Performance consultants are happy to work together with you to review your business in detail and help you optimise your payment setup. If you are interested, get in touch with your Account Manager.